Investors are abandoning cloud-software stocks amid a lack of profitability and high valuations for what had been the best-performing industry group.

The cracks began last quarter as many cloud-software, or software-as-a-service (SaaS), companies saw their shares plummet even as they beat analysts’ financial estimates. It most recently happened with Slack Technologies WORK, +2.34% and Zoom Video Communications ZM, +1.68%.

For 2020, the winners will be further separated from the losers by posting stable earnings growth.

Also from Beth Kindig: How to pick long-term stock winners in cloud computing

Shifting sentiment

Sentiment started shifting in the third quarter for SaaS companies. As a result, the First Trust Cloud Computing ETF SKYY, +0.22% has now risen 21% this year, underperforming exchange traded funds that track the broader technology market, such as the Vanguard Information Technology ETF VGT, +0.65%, which is up 36%.

YCharts

YCharts Mature cloud companies are reaching the laws of scalability, or what IDC calls the “growing base of comparison,” which says a company or a market cannot sustain high percentages of growth relative to an expanding, large market.

It’s commonly reported that slowing sales growth means cloud is slowing. Many will confuse the slowing pace of IT spending with cloud spending, but those are separate issues. For instance, the public cloud services growth rate was 4.5 times more than the IT industry overall, as reported in July 2019.

Amazon.com’s AMZN, +0.03% AWS is a great example of a how the growing base of cloud infrastructure as a service (IaaS), along with consistent profitability, is more investable than sheer revenue growth. For instance, it would be nearly impossible for Amazon to expand its current $36 billion in annualized AWS revenue at the same growth rate as when it first opened for business. In Amazon’s case, growth has gradually slowed from a peak of 81% in 2015 to a low of 35% in the most recent quarter. Some would say this is a cause for concern, when the opposite is true: AWS contributes over 71% to Amazon’s operating income.

Startups are bred to grow fast, with the average company forecasting a growth rate of 178% in revenue in the first year. Therefore, pivoting from rapid sales growth to stable profitability is not easy for tech companies as they go public.

Cloud SaaS is nearly double the market of cloud infrastructure-as-a-service and four times larger than platform-as-a-service, and this is with few large-cap heavyweights.

The large addressable market coupled with low barriers to entry has created a gold rush of SaaS startups, which is one reason Salesforce CRM, +1.60% is under more pressure than is the case in the IaaS or PaaS spaces. Salesforce, which has been on an acquisition spree, has issued lower guidance than analysts expected for the upcoming fiscal fourth quarter.

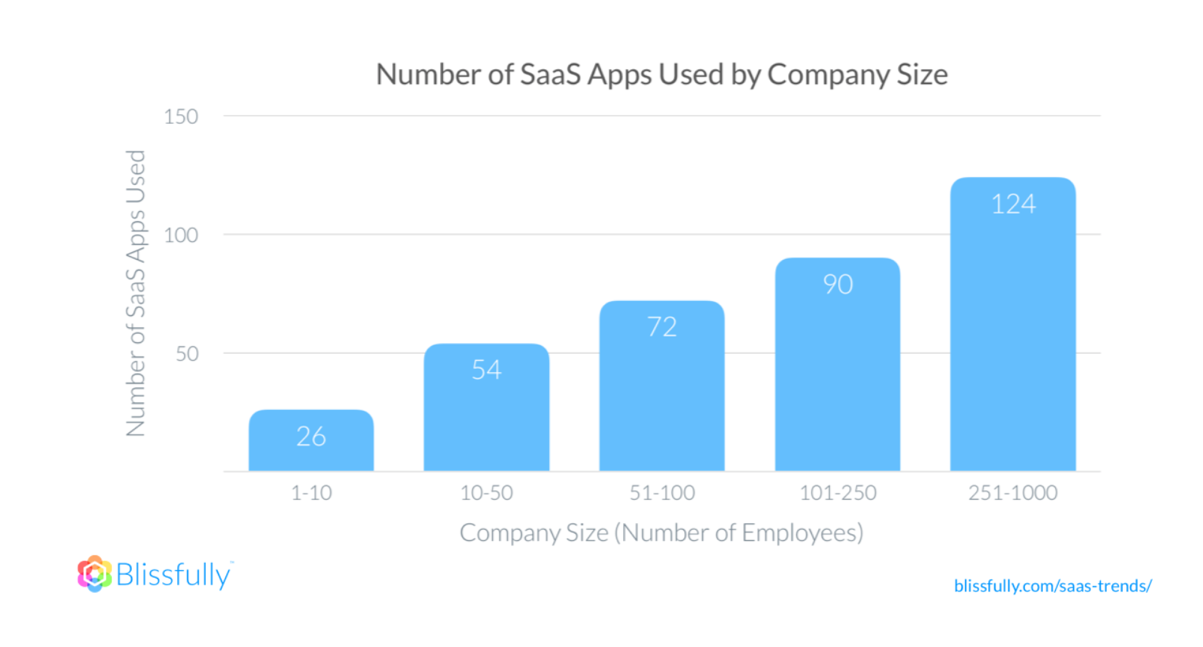

According to a survey by PriceIntelligently, competition across SaaS has increased three-fold from an average of 2.6 competitors per company five years ago to 9.7 competitors per company today. The supply of SaaS startups is driven by a voracious appetite for SaaS applications.

Companies with more than 250 employees use an average of 124 SaaS applications, while companies with up to 10 employees use an average of 26 SaaS applications. The growth rate of spending is expected to increase by 118% between 2017 and 2020. The number of subscriptions per company will increase by 95%.

Blissfully

Blissfully Because of low levels of free cash flow across many SaaS comparables, cloud software is a sector that defies traditional discounted-cash-flow modeling. To complicate matters, the overabundance of SaaS companies on both the public and private markets have varying key metrics, depending on their business model. In 2020, if the trend of the third quarter continues, the market will simplify these variables by rewarding companies that have positive and healthy EPS growth.

| Company | Ticker | Current fiscal year EPS | One year forward EPS | Expected EPS growth | EV/revenue |

| Microsoft | MSFT, +0.84% | $5.39 | $6.05 | 12% | 8.40 |

| Nutanix Class A | NTNX, +0.43% | -$2.86 | -$2.40 | 16% | 5.03 |

| Oracle | ORCL, -3.47% | $3.88 | $4.18 | 8% | 5.04 |

| SAP SE ADR | SAP, +1.32% | $5.56 | $6.00 | 8% | 5.84 |

| Slack Technologies | WORK, +2.34% | -$0.32 | -$0.21 | 34% | 20.38 |

| Splunk | SPLK, -0.10% | $1.86 | $2.31 | 24% | 10.47 |

| VMware | VMW, -3.10% | $6.58 | $7.04 | 7% | 6.40 |

| Zuora | ZUO, +0.14% | -$0.35 | -$0.27 | 24% | 5.62 |

| Five9 | FIVN, +1.40% | $0.78 | $0.86 | 11% | 12.74 |

| Salesforce.com | CRM, +1.60% | $2.90 | $3.12 | 7% | 8.61 |

| PagerDuty | PD, +3.92% | -$0.39 | -$0.24 | 40% | N/A |

| Yext | YEXT, +1.93% | -$0.51 | -$0.42 | 17% | 4.90 |

| CrowdStrike | CRWD, +4.46% | -$0.55 | -$0.21 | 62% | 23.49 |

| Zoom Video | ZM, +1.68% | $0.27 | $0.29 | 0% | 32.1 |

When looking at the chart above, we see a trend favoring positive EPS has largely played out. Microsoft MSFT, +0.84% has positive EPS, with acceptable growth and a reasonable enterprise-value-to-sales (EV/sales) ratio of 8.4. The company’s stock price is up 51% this year, more than double that of the cloud ETF.

Splunk SPLK, -0.10% also gained ground recently and is up 19% since Nov. 15, suggesting the stock was undervalued previously, given its positive and growing EPS. Five9 FIVN, +1.40% also meets the criteria of positive EPS, with guidance for 11% growth. The stock is up 50% this year.

Meanwhile, we see more confirmation that negative EPS plays a large role on the downside. CrowdStrike CRWD, +4.46% is an example of negative EPS combined with a high EV/sales valuation. The stock is down 51% from its high of $99 and is down 24% from its opening IPO price of $63.50. The company currently has one of the highest EV/sales of the companies in the table above, and at its peak in August and July, had a whopping EV/sales ratio of 61.

Lastly, Yext YEXT, +1.93% is a cautionary tale of a company with negative EPS that the market abandoned at the first sign of weakness. The company is trading 35% lower from its high in July. PagerDuty PD, +3.92% has tumbled 60% from a high in June and is down 38% from its IPO opening price of $36.75.

Notably, this could suggest Nutanix NTNX, +0.43% is exposed and may tumble with any perceived weakness.

Conclusion

Cloud software has enjoyed neck-breaking sales growth and valuations to match. On average, S&P 500 Index SPX, +0.01% member companies, excluding energy, are reporting an aggregate of 5.2% revenue growth in the current quarter. Many cloud-software companies are reporting 10 to 20 times that.

Despite such fast growth, investors are leery of companies with neck-breaking revenue growth, such as Okta OKTA, +3.04%, Yext and CrowdStrike. Instead, we see ample evidence that positive EPS with at least 10% forward growth is attractive to investors. And there’s no reason to believe that trend won’t spill into next year.

The writer owns shares of Microsoft, Slack and Zoom.

Beth Kindig is a San Francisco-based technology analyst with more than a decade of experience in analyzing private and public technology companies. Kindig publishes a free newsletter on tech stocks at Beth.Technology and runs a premium research service.

div > iframe { width: 100% !important; min-width: 300px; max-width: 800px; } ]]>