(Bloomberg Opinion) — Prosus NV’s latest bid to acquire food delivery specialist Just Eat Plc was still little more than an appetizer.

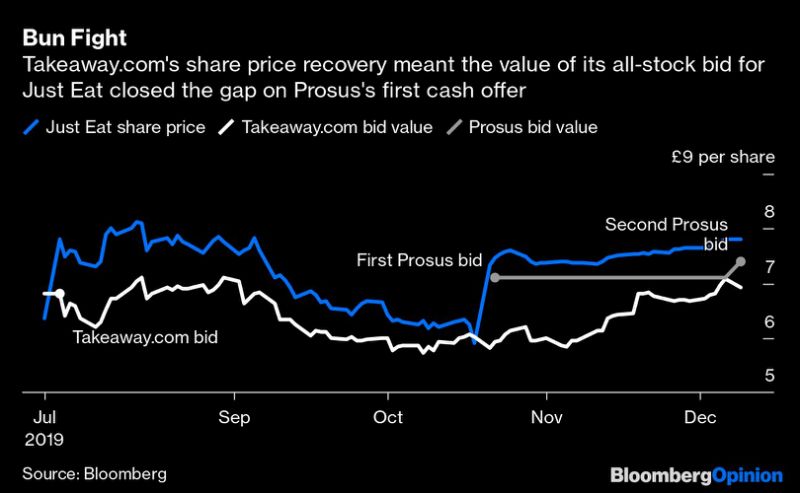

The Amsterdam-based technology investment firm raised its offer a measly 4.2% to 740 pence-per-share, while lowering the acceptance threshold to 50%. It had little alternative but to increase the value of its proposal: the recent recovery in shares of counterbidder Takeaway.com NV meant that company’s all-stock offer had closed the gap to Prosus’s cash bid, while offering the potential for more upside from the combined entity.

The new bid, which was unanimously rejected by the Just Eat board on Tuesday, nonetheless increases the pressure on the Takeaway.com bid as it nears its Dec. 11 deadline for investors to tender their Just Eat stock.

Just Eat shares have been trading above 780 pence, higher than both offers. Investors are still expecting a main course — in the form of more generous bids — and they’re right to do so. Takeaway.com’s initial offer back in July looked mightily opportunistic. It could think about giving Just Eat shareholders more of the combined company, up from the current offer of 52%. Prosus’s net cash position means it has plenty of scope to return with a higher bid.

Even with the new bid, Just Eat still looks cheap. The Prosus offer values it at just 22 times predicted 2020 Ebitda. Takeaway.com and U.S. peer GrubHub Inc. are valued at 60 times and 32 times forward earnings respectively. Both of Just Eat’s suitors should be able to offer more without riling their own investors.

For sure, the British firm has its problems. It faces heightened competition in its home market from Uber Technologies Inc.’s food delivery arm and Deliveroo, which is seeking regulatory approval for a massive cash injection from Amazon.com Inc. It’s also been slow to build out captive delivery networks, which can help attract new restaurants and foster growth (albeit at the cost of short-term profitability).

But there’s a reason that the bun fight is over Just Eat, rather than Deliveroo, which has been up for sale at various times over the past 18 months. Just Eat enjoyed an operating profit of 124 million pounds ($163 million) on sales of 780 million pounds last year, while Deliveroo endured a 257 million-pound loss on revenue of just 476 million pounds. Yet the smaller firm was still seeking a valuation of more than 4 billion pounds in its most recent private fundraising round.

With each passing month at the center of the takeover scrap, Just Eat risks losing out to its rivals, not least because it has yet to appoint a permanent CEO after the departure of Peter Plumb in January. If neither bidder emerges victorious by their respective deadlines (Dec. 11 for Takeaway.com; Dec. 27 for Prosus), then perhaps the U.K.’s Takeover Panel will step in to create a formal auction and seek final bids.

As it stands, Just Eat investors have good reason to ask for a bigger sweetener.

To contact the author of this story: Alex Webb at [email protected]

To contact the editor responsible for this story: Melissa Pozsgay at [email protected]

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe’s technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com/opinion” data-reactid=”31″>For more articles like this, please visit us at bloomberg.com/opinion

©2019 Bloomberg L.P.