Gold traders wondering about bullion’s 5% decline since its February high may not need to look any further than the calendar. That’s because gold appears to follow a six-months-on, six-months-off seasonal pattern. We’re right in the middle of the period of seasonal weakness, which likely could last through August.

To be sure, this seasonal pattern doesn’t always hold up every year. Its existence is evident in terms of averages over many decades. But it certainly has held up this year.

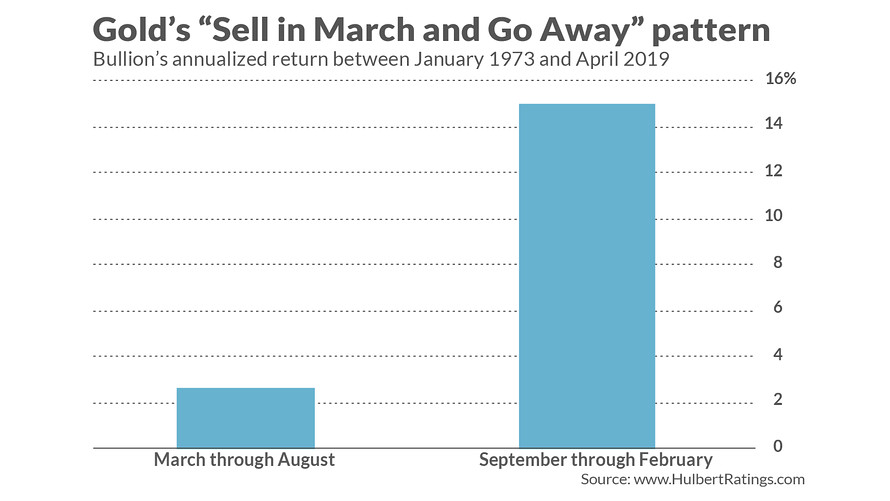

Since 1973, when gold GCM9, +0.08% began freely trading, bullion has produced an annualized return of 15.0% from September through February, versus 2.7% from March through August. (See accompanying chart.) This difference is statistically significant at the 95% confidence level that statisticians often use when determining if a pattern is genuine.

The first academic study that documented this seasonal effect, as far as I can tell, was conducted by Dirk Baur, a professor of accounting and finance at the University of Western Australia business school. Gold price behavior in the seven years since constitute an out-of-sample test. That’s crucial from a statistical point of view, since out-of-sample tests help reduce the possibility that the original finding was the result of nothing more than what statisticians refer to as “data snooping.”

In this case, the pattern has held up nicely. Since 2012, gold during the seasonally favorable six-month period has produced a return that is 10.1 annualized percentage points better than in the six-month unfavorable period. That’s almost as large as the difference in the pre-2012 sample.

Why would gold follow this seasonal pattern? Baur has speculated about several possible causes, including jewelry demand in India prior to Denali (that country’s annual “festival of lights” that occurs during autumn) and gold investors’ anticipation of the “Sell in May and Go Away” pattern in the stock market.

Don’t forget, however, that seasonal factors aren’t the only factor that makes the gold world go ‘round. Fundamental factors such as interest rates and inflation obviously play a role, as does market sentiment. So you shouldn’t trade into and out of gold solely on the basis of this seasonal pattern.

Furthermore, notice that, even though gold historically has produced a much lower return in the March-through-August period than in the other six-month period, its return has still been slightly positive. So you could very well decide that, after taking taxes and other transaction costs into account, this seasonal pattern is not important enough to follow.

But, if you were otherwise getting into or out of the gold market, and therefore incurring those transaction cots, you might want to take this seasonal pattern into account.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at [email protected]

More: Here are the stocks to buy if an all-out U.S.-China trade war erupts, says Goldman