Rainbow, North East England.

Owen Humphreys/Zuma Press

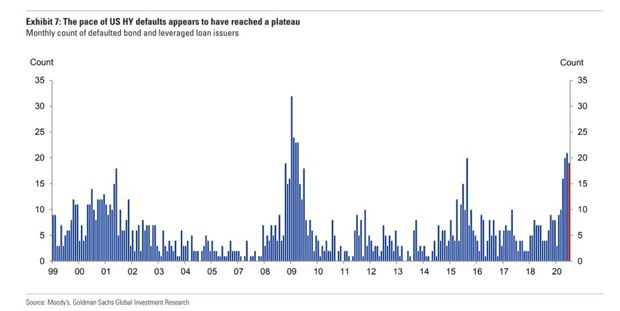

Goldman Sachs has gotten on the bandwagon in terms of thinking defaults by speculative or “junk” rated U.S. companies won’t get a whole lot worse this year.

Analysts at the bank this week cut their default forecast for the sector to 10.5% from 13% for the full year, noting that after a blistering three months, defaults by speculative or “junk” rated companies likely have plateaued.

The Goldman GS, -0.20% team, led by Lotfi Karoui, said that meeting their prior projection, based on the current 8.4% default rate for both U.S. high-yield bonds and loans “would essentially require the current pace of monthly defaults to persist for the remainder of the year,” in a late Thursday note.

“While this scenario is quite plausible, we do not think it captures the most likely outcome given the current reality of macro fundamentals.”

The cluster of monthly defaults seen since the onset of the pandemic in the U.S. has been the worst patch for debt-laden businesses since the global financial crisis.

While the virus remains a threat, the U.S. has unleashed trillions worth of fiscal and monetary stimulus, including its first stab ever at buying corporate debt, to help offset the economic shocks of the coronavirus pandemic on American businesses, households and municipalities.

Related: A binge? Bulge? Or just the new normal for debt in America as Fed helps spur string of records

And while Washington remains in a stalemate over another pandemic aid package, investors remain confident that Congress will end up spending more to help shore up Covid-battered parts of the U.S. economy until the virus is better contained.

“Small businesses, in particular, need more help,” said Nichole Hammond, a senior portfolio manager focused on high-yield at Angel Oak Capital Advisors, in an interview.

But while some high-yield bond issuers keep testing new, sub-3% lows in terms of coupons paid to investors, that doesn’t mean the entire market is in an feverish risk-on mode.

“Certain subsectors we are avoiding,” Hammond said, pointing to theaters and companies focused on producing live events. “We also are negative on retail. The pandemic is accelerating secular trends in that sector.”

High-yield bonds are priced at a spread over U.S. Treasurys TMUBMUSD10Y, 0.709%, which were largely unchanged for the week at 510 basis points over the risk-free benchmark, according to BofA Global data. Junk bonds also often track the tone of U.S. stocks, which saw the major benchmarks book further weekly gains, while the S&P 500 index SPX, -0.01% ended Friday’s session just shy of its prior record close in February.

With the “avalanche” of recent debt financings in the U.S. high-yield bond market, BofA Global analysts said they expect bond issuance to hit a record $350 billion for the year, or 10% above the prior annual peak in 2012, in a note Friday.

But with their low yields, BofA analysts also said the “high-yield bond market may soon need a new name that better reflects the new reality.”

Related: Can the Fed tame an avalanche of corporate distress? Bond investors are betting on it