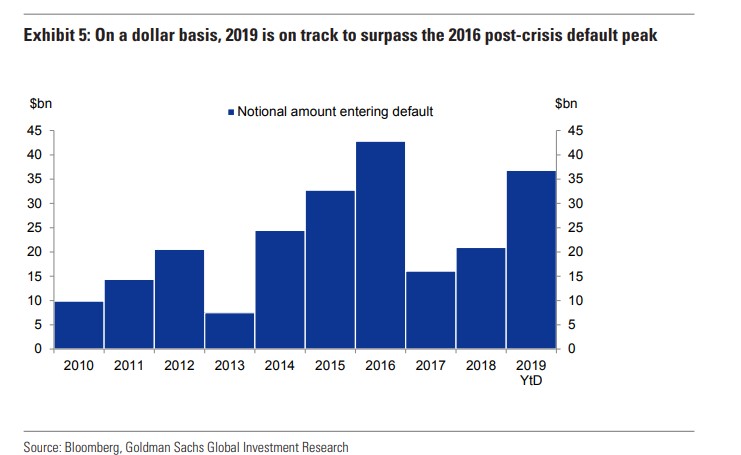

Defaults on bonds issued by debt-laden U.S. companies with speculative-grade ratings are on pace to reach a new high this year for the post 2008 crisis era, according to Goldman Sachs analysts.

The bank has tracked more than $36 billion of defaulted so-called “junk bonds” already in 2019, and there are likely to be more, particularly in the energy sector, to eclipse the prior post crisis default record of $43 billion in 2016, wrote Goldman analysts led by Lotfi Karoui in a Thursday note to clients.

“Thus far, defaults have been highly concentrated among energy issuers, a trend that reflects structural as opposed to cyclical challenges,” the Goldman analysts wrote. “The lingering weakness in oil prices coupled with weak growth sentiment may push issuers in other structurally-challenged sectors toward defaults.”

Oil field servicing company Weatherford International Ltd WFTIQ, -0.11%, which filed for bankruptcy with $7.4 billion of high-yield debt, is the year’s second-largest default, after the massive default of California’s Pacific Gas and Electric Company PCG, -0.76% on $18.3 billion of debt in January, according to Moody’s Investors Service.

In the case of Weatherford, Moody’s said it expects to see bond recoveries of 35%-65% on roughly $5.85 billion of debt that the company hopes to slash through its restructuring.

PG&E was considered an investment-grade credit, until it filed for bankruptcy following devastating California wildfires in 2017 and 20180 left it facing billions in potential liabilities.

This chart shows the dollar amount of defaulted U.S. high-yield bonds thus far in 2019, which is approaching levels not seen since 2016, after Brent crude oil prices plunged below $35 per barrel and put significant pressure on the financial conditions of oil companies and exporters.

Goldman Sachs

Goldman Sachs

Moody’s said this week in a separate report that junk-bonds issued by companies in July came with the worst protections yet for investors.

Check out: Junk bonds are getting worse and investors are starting to take notice

At present, the three-month trailing high-yield bond default rate is above 5% on an annualized basis, a sharp jump from its 1.3% bottom in November 2018, according to Goldman analysts.

By comparison, the default rate traveled north of 14% for U.S. high-yield bonds in the aftermath of the 2007-2008 global financial crisis, according to Moody’s, which said in July that its baseline forecast was for defaults to stay below 4% through July 2020.

Goldman analysts also don’t see defaults moving meaningfully higher from current levels, absent a “full-blown recession,” which the bank’s U.S. economics team doesn’t anticipate occurring in the near term.

Recession and trade war jitters rattled U.S. stocks this week, although the major benchmarks managed to close higher on Friday, with the Dow Jones Industrial Average DJIA, +1.20% adding 300 points, and the S&P 500 index SPX, +1.44% gaining 41 points and the Nasdaq Composite Index COMP, +1.67% increasing by 308 points.

Investors have plenty of high-risk and so-called grey swan events to watch for, as the third quarter draws closer.

In high-yield, a big focus will be corporate earnings through year-end. Companies can end up in default when earnings slump, making it harder for borrowers to keep up on debt payments.

And with energy making up 14% of the closely-tracked Bloomberg Barclays U.S. high-yield bond Index, Oxford Economics is keeping a close eye on the fortunes of energy companies.

“Our main source of worry is the fact that the improvement in U.S. fundamentals since 2017 can be entirely attributed to the energy sector,” wrote Michiel Tukker, Oxford Economics’ global strategist in a note Friday.

“It is telling that oil hasn’t risen despite OPEC cuts and tensions in the Gulf of Hormuz,” Tukker added.

October Brent crude BRNV19, +0.00% finished up 0.7% on Friday to $58.64 a barrel on ICE Futures Europe, but was still sharply down from its two-year high of $86.29 on October 3, 2018, according to FactSet data.

Check out: Oil prices settle higher for the day and the week

What’s more, Tukker found that 18% of U.S. high-yield companies recently reported negative hearings, the highest since the global financial crisis outside of the oil price collapse in 2014 and 2015.

Tukker said that could drag down the sector’s debt interest coverage ratios, a measure of corporate earnings to interest expenses.

“With earnings outlook gloomy, we expect the ratio to fall significantly going forward, bringing interest coverage ratios down rapidly.”