The semiconductor giant has lost momentum on the stock market of late, but investors would do well to look at the bigger picture.

Nvidia (NVDA -0.03%) announced fiscal 2025 second-quarter results (for the three months ended July 28) on Aug. 28, and the stock has shed 18% of its value since then, despite delivering better-than-expected results along with guidance that exceeded consensus expectations.

Investors are probably worried about the fact that Nvidia forecast year-over-year revenue growth of 80% in the current quarter to $32.5 billion. While that’s impressive, it is lower than the 122% growth it recorded in the previous quarter. Additionally, the growing concerns about the sustainability of massive investments in artificial intelligence (AI) technology seem to be giving Nvidia investors another reason to be skeptical about the stock’s future.

With the stock having more than doubled in 2024, is now the time for Nvidia investors to start booking profits? Or should they continue holding the stock to wait for the bearish sentiment to get over? Or will it be a good idea to use the dip in Nvidia stock to buy more shares?

Reasons to buy Nvidia stock

Nvidia has a solid moat in the markets it serves. For example, the company enjoys a healthy share of more than 80% in the AI chip market, and this has been central to its stunning growth in recent quarters. Nvidia’s dominant position in AI chips is the reason why its data center revenue increased an impressive 154% year over year last quarter to a record $26.3 billion.

That number is way higher than the next prominent player in the market for AI accelerators — Advanced Micro Devices — which recorded $2.8 billion in data center revenue last quarter (including sales of server central processing units). AMD expects to end the year with more than $4.5 billion in revenue from sales of AI GPUs, which means Nvidia is leagues ahead of its closest rival in this market.

This moat explains why the pull of Nvidia’s AI chips is so strong. Customers are still willing to purchase GPUs manufactured on the Hopper architecture, which was announced two and a half years ago, even though its next-generation Blackwell chips are set to enter production next quarter.

Nvidia has generated almost $49 billion in data center revenue in the first half of the current fiscal year, indicating that it could finish the year with almost $100 billion in revenue from this segment. John Vinh of KeyBanc estimates that Nvidia’s data center revenue could jump to $200 billion next year thanks to the arrival of its Blackwell chips.

While that looks like an ambitious forecast, it won’t be surprising to see Nvidia indeed hitting that mark. The company’s data center business is more than doubling each quarter, and it points out that the demand for its Blackwell chips will outpace supply, a trend that the chipmaker expects to continue in the next fiscal year as well.

Throw in the fact that Nvidia’s foundry partner is boosting capital expenditures and increasing its manufacturing capacity, and there is a good chance that the company could indeed enjoy a big data center boost in 2026 as well.

Consensus estimates are projecting Nvidia’s revenue to increase to $161 billion in fiscal 2026, but it could significantly exceed that mark if its data center business doubles once again. So there is a good chance that Nvidia’s results in the upcoming quarters could be better than expectations. That could help the stock regain its mojo, which is why it would be a good idea to buy it while it is down.

Reasons to hold

The biggest factor that could keep investors from adding more Nvidia stock to their portfolios even after its pullback is its valuation. It is trading at an expensive 28 times sales, which is higher than the U.S. technology sector’s average of 7.8. Additionally, the company’s trailing price-to-earnings ratio of 50 is also higher than the sector average of 44.

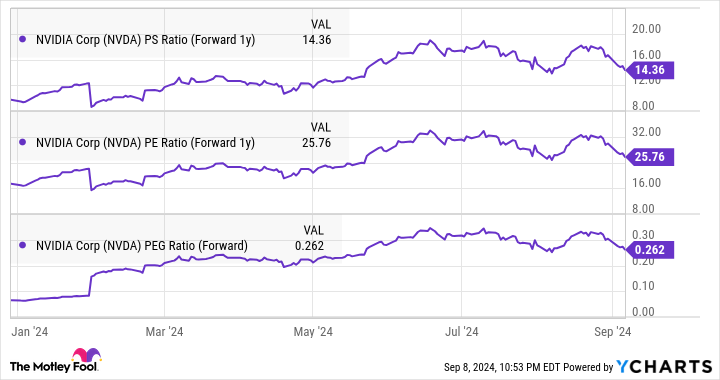

So opportunistic investors may be waiting for Nvidia to become cheaper and would want to hold on to their current positions. Nvidia may get cheaper if the sell-off continues, but investors shouldn’t miss the fact that this semiconductor stock is indeed cheap when we consider the pace at which it is growing. This is evident from the chart.

NVDA PS Ratio (Forward 1y) data by YCharts

The stock’s forward earnings multiples are much lower than its trailing multiples, pointing toward a nice bump in its revenue and earnings. Meanwhile, Nvidia’s price/earnings-to-growth ratio (PEG ratio) — which is a forward-looking valuation metric that takes into account a company’s growth potential — is significantly lower than 1. A PEG ratio of less than 1 means that a stock is undervalued considering the growth that it may deliver.

That’s the reason why investors who are holding off from buying more Nvidia stock right now in anticipation of a more attractive valuation should not wait too long and consider acting before it starts heading higher.

Reasons to sell

The discussion so far suggests that Nvidia’s recent sell-off doesn’t seem justified, considering the potential growth it is likely to deliver on account of its strong position in the AI chip market, as well as the company’s valuation that can’t be called expensive based on its phenomenal growth.

However, one reason why investors may want to sell Nvidia right now is if they want to get in on the stock at a lower price later on. Assuming someone sold some of their Nvidia holdings before the results were out, they would be able to buy more stock now, and that too at a more attractive valuation.

While this does seem like a good strategy at first, timing the market isn’t exactly a smart thing to do, as buying and holding on to solid companies over a long period is a tried-and-tested strategy of making money in the stock market.

So, there isn’t exactly a strong reason to sell Nvidia right now. Moreover, the reason for investors to hold off from buying more Nvidia shares doesn’t hold much water either. Investors would do well to buy Nvidia following its latest drop, as the bull case appears to be solid enough to warrant an investment.