We’ve been bearish on Netflix NFLX, +0.70% for many years, not because the firm provides a poor service, but because it cannot monetize content as well or sustain investment in content for as long as its competitors. Though the stock has only become more overvalued, our bearish thesis is proving truer by the day.

With its huge subscriber miss in the first quarter and weak guidance for subscriber growth, the weaknesses in its business model are undeniable. As a growing number of competitors take market share at a rapid rate, it’s clear that Netflix cannot generate anywhere close to the profits implied by the current stock price.

We think the stock at best is worth just $231 today – a 54% downside. And even that might be optimistic.

The new normal: Losing market share

Netflix reported just under 4 million new subscribers in the first quarter, well below its previous guidance of 6 million and consensus expectations of 6.3 million. Management guided for just one million subscriber additions in 2Q21, which puts Netflix on the lowest subscriber addition trajectory since 2013, or when Netflix began producing original content

Read: Netflix’s underwhelming subscriber gains spark ‘vigorous debate’ about the future

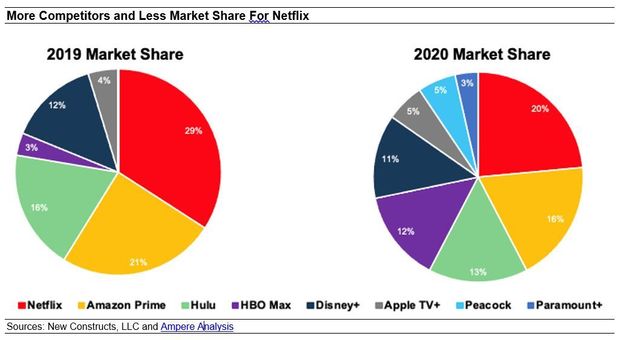

Netflix can claim, as management did in its earnings press release, that competition didn’t play a large role in the subscriber miss, but market share data for the streaming industry indicates otherwise. According to a report by Ampere Analysis, a media and content analytics firm, Netflix’s share of the U.S. streaming market fell from 29% in 2019 to 20% in 2020. This chart shows Netflix lost a lot of market share and gained a lot of competitors in 2020.

We expect Netflix will continue to lose market share as more competitors enter the market and deep-pocketed peers like Disney DIS, +0.15% and Amazon AMZN, +1.10% continue to invest heavily in streaming. For reference, Disney+ expects to add about 35 million to 40 million subscribers a year through 2024, while Netflix, based on its 2021 trajectory (Netflix expects to add just 5 million subscribers in the first half of 2021), will only add around 10 million subscribers per year through 2024.

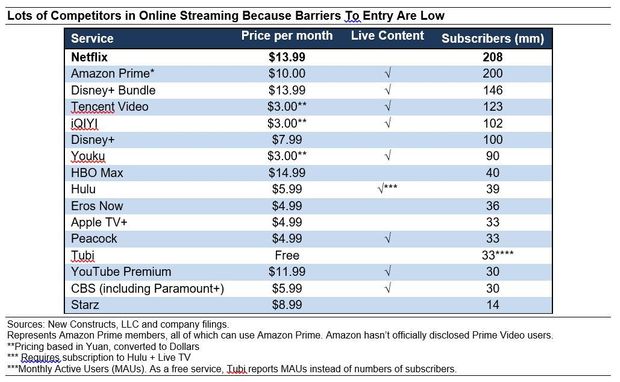

The streaming market is now home to at least 14 streaming services with more than 10 million subscribers. Many of these competitors (like Disney, Amazon, YouTube (owned by Google parent Alphabet GOOG, +1.04% GOOGL, +0.98% ), Apple AAPL, +1.28%, Paramount VIAC, -2.43% and AT&T’s T, +1.19% Warner Bros.) have profitable businesses that can subsidize lower-cost streaming offerings and permanently reduce Netflix’s subscriber growth potential.

Top-line and bottom-line pressures

We underestimated Netflix’s ability to raise prices while maintaining subscription growth because we expected competitors to enter the streaming market sooner. But now that the competition is here, our thesis is playing out as expected. As a result, consumers have a growing list of lower-cost alternatives to Netflix and may not be as willing to accept price hikes going forward.

Increased competition hasn’t only hurt subscriber growth, market share and pricing power. It also raises the costs for the company to produce, license and market its content.

At the same time, Netflix is paying more than ever to acquire subscribers. Marketing costs and streaming content spending has risen from $308 per new subscriber in 2012 to $565 per new subscriber over the trailing 12 months (TTM).

For a user paying $14 per month in the U.S., it takes Netflix over three years to break even. It takes nearly five years to break even on international users, where Netflix is seeing the most subscriber growth.

Competition creates a Catch-22: Growth or profits, but not both

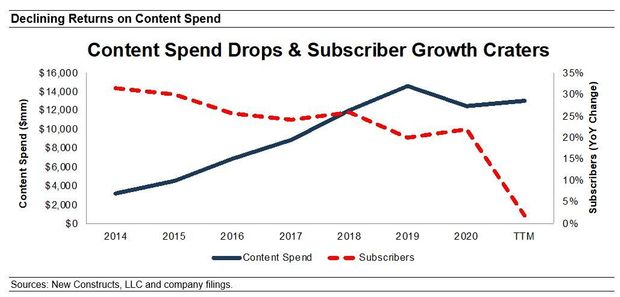

Netflix’s free cash flow was positive in 2020 because the firm cut content spending. But not growing content spending in 2020 resulted in subscriber growth cratering.

So Netflix plans to spend $17 billion on new content in 2021….but will it work? The data suggests “no” and that throwing billions of dollars at content will not be enough to fend off its competition.

Here is where Netflix narrative breaks down: the content spending cuts needed to be profitable prevent Netflix from achieving the scale (i.e. number of subscribers) needed to justify its lofty valuation.

So far, spending billions on original content may win some awards, but subscribers still like licensed content more. For example:

- Just 3% of viewed minutes was spent on Netflix-produced shows

- Its three most-streamed series in 2020 were licensed

Netflix’s shift to original content was a bet that it could wean viewers off licensed content and forgo the costly (and ongoing) license fees. Original content, in general, can be cheaper than licensed content, but that advantage only translates to profits if it is as least as popular, which it is not.

Consequently, Netflix must continue to invest a significant amount of money in its licensed content library, such as the $500 million deal for “Seinfeld” and the more recent deal with Sony Pictures, rumored to cost $1 billion.

On top of all that, Netflix, unlike its competitors, doesn’t have any live sports offerings to keep subscribers hooked.

The real problem: Limited ability to monetize content

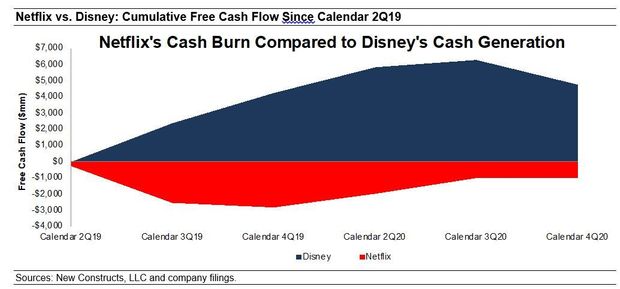

Netflix has one revenue stream, subscriber fees, while Disney monetizes content across its theme parks, merchandise, cruises and more. Competitors such as AT&T and Comcast/NBC Universal CMCSA, +1.01% generate cash flows from other businesses that can help fund streaming platforms.

As a result, Netflix loses money while competitors make money. This chart compares Netflix’s cash burn to Disney’s cash generation. Since the second quarter of 2019, Netflix has burned $1 billion in free cash flow while Disney generated $4.7 billion in FCF. Netflix burned $11.7 billion in FCF over the past five years.

The stark contrast raises the question of how long Netflix can keep this up. We don’t think Netflix’s money-losing mono-channel streaming business has the staying power to compete with Disney’s (and all the other video content producers’) original content spending—at least not at the level to grow subscribers and revenue at the

Netflix’s valuation requires twice the combined revenue of Fox and ViacomCBS

We use our reverse discounted cash flow (DCF) model and find that the expectations for Netflix’s future cash flows look overly optimistic given the competitive challenges above and guidance for slowing user growth. To justify Netflix’s current stock price of around $505, the company must:

- Maintain its record 2020 margin on net operating profit after taxes (NOPAT) of 16% (vs. five-year average of 9% and three-year average of 12%) and

- Grow revenue 14% compounded annually for the next decade, which assumes revenue growth at consensus estimates in 2021-2023 and 13% each year thereafter

In this scenario, Netflix’s implied revenue in 2030 of $89.4 billion is more than 3.5 times its 2020 revenue, double the combined TTM revenue of Fox Corp. FOXA, +3.38% and ViacomCBS and 47% greater than Disney’s TTM revenue. See the math behind this reverse DCF scenario.

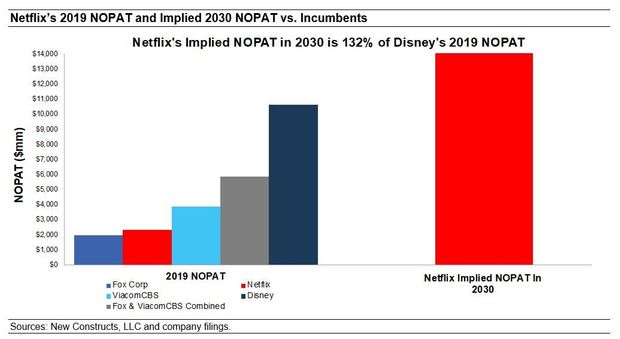

Netflix’s NOPAT in this scenario is over $14 billion in 2030, or over 3.5 times its 2020 NOPAT. To justify its current price, Netflix’s profits must grow to 132% of Disney’s 2019 NOPAT, as this chart shows.

Netflix is worth just $231 per share if profit margins can’t be sustained

Below, we use our reverse DCF model to show the implied value of NFLX under a more conservative scenario that reflects a more realistic assessment of the mounting competitive pressures on Netflix. Specifically, we assume:

In this scenario, Netflix’s NOPAT in 2030 is over nearly $8 billion (nearly twice 2020 NOPAT) and the stock is worth just $231 today – a 54% downside to the current stock price. See the math behind this reverse DCF scenario.

Both scenarios might be optimistic

Each of the above scenarios assumes Netflix’s YoY change in invested capital is 10% of revenue (same as 2020) in each year of our DCF model. For context, Netflix’s invested capital has grown 40% compounded annually since 2013 and change in invested capital has averaged 24% of revenue each year since 2013.

Clearly, assuming the YoY change in invested capital of revenue stays at just 10% is very conservative. We think spending will need to be much higher to achieve the growth that we forecast. Nevertheless, we use this lower assumption to underscore the risk in this stock’s valuation.

David Trainer is the CEO of New Constructs, an independent equity research firm that uses machine learning and natural language processing to parse corporate filings and model economic earnings. Kyle Guske II and Matt Shuler are investment analysts at New Constructs. They receive no compensation to write about any specific stock, style or theme. New Constructs doesn’t perform any investment-banking functions and doesn’t operate a trading desk. This is adapted from a report entitled “Netflix: A Meme-Stock Original.” Follow them on Twitter @NewConstructs.