This stock could be a winner in the long run thanks to the central role it is playing in the increasing adoption of fast-growing technologies such as artificial intelligence.

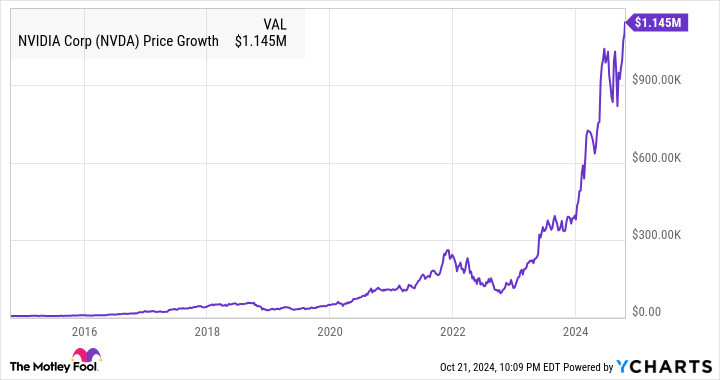

Nvidia has turned out to be an outstanding investment in the past decade, as shares of the company have shot up a whopping 32,600% during this period and outpaced the 207% gains clocked by the S&P 500 index.

So, an investment of just $3,500 made in shares of Nvidia a decade ago is now worth just over a million dollars.

Nvidia, therefore, has turned out to be a millionaire-maker stock over the past 10 years, assuming someone put $3,500 into its shares at that time and never sold. However, as the chart above shows, the majority of Nvidia’s gains have come in the past couple of years when the artificial intelligence (AI) craze gripped the globe.

Nvidia has been at the forefront of the AI revolution thanks to its graphics processing units (GPUs), which have been instrumental in training AI models and are now being deployed for AI inference. The good part is that Nvidia can keep growing at a healthy pace in the future as well thanks to the lucrative opportunity present in the AI chip market, a space where it is the dominant player right now.

But at the same time, investors looking to buy Nvidia stock right now will have to pay a hefty 65 times earnings and 36 times sales. While Nvidia could justify that valuation with its stunning growth, investors looking for an alternative that’s trading at relatively cheaper levels would do well to take a closer look at Taiwan Semiconductor Manufacturing (TSM 2.78%), popularly known as TSMC.

The Taiwan-based foundry giant plays a critical role in the global-semiconductor market and could be an ideal pick for investors looking to construct a million-dollar portfolio. Let’s look at the reasons why.

TSMC is one of the best ways to play the AI boom

TSMC is the world’s largest-semiconductor foundry. Its fabrication plants are used by top chipmakers such as Nvidia, AMD, Broadcom, Qualcomm, and many others to manufacture chips. Additionally, consumer-electronics giant Apple is TSMC’s largest customer, while the likes of Sony also turn to the Taiwanese company for their chip manufacturing.

It is worth noting that TSMC ended 2023 with an impressive base of 528 customers, manufacturing close to 12,000 products for multiple-end markets, such as smartphones, the Internet of Things (IoT), high-performance computing, consumer electronics, and automotive. Given that AI is driving solid growth across all these end markets, it is not surprising to see why TSMC has been growing at an incredible pace of late.

The company released third-quarter 2024 results on Oct. 17, reporting a 36% year-over-year increase in revenue to $23.5 billion. That exceeded the higher end of the company’s $23.2 billion guidance. Even better, TSMC’s net profit shot up 54% year over year to $10.1 billion, easily clearing the consensus estimate. The stronger growth in the company’s earnings can be attributed to an increase of 4.2 percentage points in its net-profit margin.

TSMC’s outstanding growth was driven by the growing demand for the company’s advanced chip nodes, which are 7-nanometer (nm) or smaller in size. More specifically, the advanced-process nodes produced 69% of its total revenue as compared to 59% in the year-ago period. What’s worth noting here is that TSMC’s 3nm node accounted for 20% of its top line in the previous quarter as compared to just 6% in the year-ago quarter.

This can be attributed to the arrival of the latest generation of Apple’s iPhones, which sport a 3nm processor manufactured by TSMC. Looking ahead, the company’s 3nm process node should continue to witness stronger adoption as next-generation AI chips from Nvidia, AMD, and Intel are expected to be manufactured using this platform.

What’s more, TSMC is pushing the envelope further as it is currently developing its 2nm technology, which is expected to go into production next year. So, TSMC will have an additional advanced node to sell to customers, and it won’t be surprising to see the 2nm process becoming another solid-growth driver for the company.

That’s because chips manufactured using a smaller-process node pack more transistors into a smaller surface area and have higher-computing power and thermal efficiency. As a result, customers have been using TSMC’s advanced-process nodes to manufacture chips capable of delivering superior performance while keeping power consumption low.

With a market share of almost 62% in the global-semiconductor foundry space, which is well ahead of second-placed Samsung’s 11%, TSMC is in an outstanding position to capitalize on the secular growth of the semiconductor market in the long run. That’s precisely why its guidance for the current quarter is outstanding as well.

TSMC is expecting $26.5 billion in revenue in Q4 at the midpoint of its guidance range, along with an operating margin of 47.5%. Its top-line forecast points toward a potential increase of 35%, while the bottom line should also increase at a nice clip considering that TSMC’s operating margin stood at 41.6% in the prior-year quarter.

However, investors looking to construct a million-dollar portfolio would do well to focus on the company’s long-term growth potential as well.

Why TSMC looks like a good fit for a million-dollar portfolio

The global-semiconductor market is expected to generate $1.47 trillion in revenue in 2030, up from $729 billion in 2022. Not surprisingly, the global-semiconductor foundry market is set to jump from $122 billion last year to $276 billion in 2033. We have already seen that TSMC is the dominant player in this space, but more importantly, the company has significantly expanded its addressable market of late by diversifying beyond the foundry space.

Under its new Foundry 2.0 business model, TSMC has moved into additional markets that include “packaging, testing, mass making, and others.” The company points out that this new model has increased its addressable market from $115 billion to $250 billion already. So, there is a solid chance of TSMC sustaining its impressive growth rates for a long time to come.

Analysts are expecting the company to finish 2024 with $89.3 billion in revenue, which would be a 28% increase from last year. The following chart indicates that TSMC would be able to sustain impressive growth for the next couple of years as well.

TSM Revenue Estimates for Current Fiscal Year data by YCharts.

However, the chart also shows that analysts have been bumping up their revenue estimates for TSMC, a trend that could continue because of the company’s expanded-addressable market and the secular growth of the foundry space over the next decade. That’s why investors would do well to buy this semiconductor stock right away as it is trading at an attractive 35 times trailing earnings and 25 times forward earnings, which makes it significantly cheaper than Nvidia.

Another thing worth noting is that TSMC stock has jumped over nine times in the past decade. It may get close to replicating such a performance in the future based on the points discussed above, which is why anyone looking to make a million-dollar portfolio should consider buying it before it soars higher.