Broadcom is approaching the mark few companies have ever achieved.

Broadcom (AVGO 2.76%) has risen to near the top of the pyramid when it comes stocks that are considered strong artificial intelligence (AI) investments. While it isn’t quite to the level of Nvidia, it’s likely just a tier or two below it. Broadcom is an enormous company, currently worth around $780 billion.

That means it’s a stone’s throw away from achieving the illustrious $1 trillion market capitalization, as it only needs to rise just shy of 30% to achieve this impressive feat. But could it do this in 2025? Let’s take a look.

Broadcom’s growth figure is highly skewed

It isn’t easy to summarize Broadcom’s work because it does so much. It offers its clients hardware and software solutions in various industries and chip design services. On the hardware side, its networking switches have gotten a lot of attention, as these devices are critical in building out data centers meant to train AI models.

On the software side, Broadcom has products that allow businesses to control their mainframe computers, which is critical in today’s increasingly digital business environment. It also has cybersecurity software, but its biggest software product came from an acquisition.

Last year, Broadcom purchased VMware, which allows its users to establish a virtual desktop on the cloud. This has been a successful acquisition, and it’s the primary reason why Broadcom grew revenue in its latest quarter.

In its fiscal 2024’s third quarter (ended Aug. 4), Broadcom’s revenue rose 47% year over year to $13 billion. While that sounds impressive, what’s going on under the hood is far less so. If you subtract out the effect of the VMware acquisition (which didn’t contribute to the year-earlier results), revenue only rose 4%. That’s a substantial change and completely modifies how investors might look at Broadcom.

But that doesn’t mean AI isn’t helping Broadcom’s business. CEO Hock Tan said this during Broadcom’s Q3 earnings call:

As you know, our hyperscale customers continue to scale up and scale out their AI clusters. Custom AI accelerators grew three-and-a-half times year on year. In the fabric, Ethernet switching, driven by Tomahawk 5 and Jericho3-AI grew over four times year on year, while our optical lasers and thin dies used in optical interconnects grew threefold.

When you break that down, that’s some incredible growth. Connectivity switches grew 400%, while custom AI accelerators, such as Alphabet‘s Tensor Processing Unit (TPU), which provides better AI performance than an Nvidia GPU, were up 350%!

These parts of Broadcom were strong; the problem is that they don’t make up an outsized portion of its business, so the effect these segments are having is muted. But that could change next year.

Broadcom is slated for another strong year

For fiscal 2025, Wall Street analysts expect Broadcom’s revenue to increase by 17% year over year. That figure includes a fully integrated VMware, so it accurately portrays the true revenue growth picture. Furthermore, earnings per share (EPS) are projected to increase from $4.82 this year to $6.17 next year, a 28% rise.

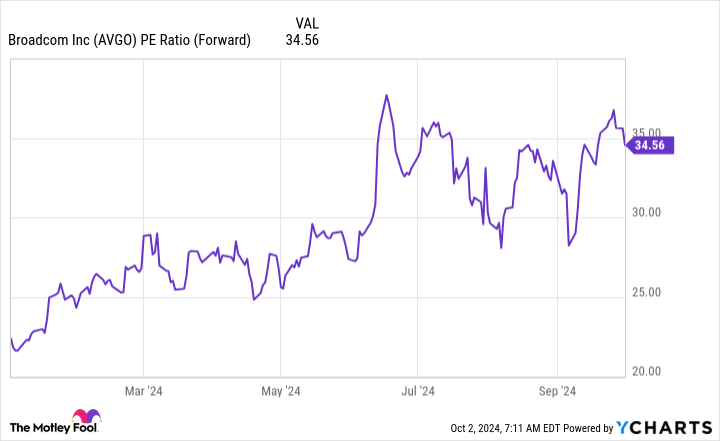

That looks like a great company to invest in if investors can pay a reasonable price for the stock. But at 35 times forward earnings, Broadcom is a bit pricey.

AVGO PE Ratio (Forward) data by YCharts

With Nvidia trading at 41 times earnings and growing much faster, it’s also in the same valuation realm. So investors must determine if they need to search for the next Nvidia in Broadcom, or if they should just stick with Nvidia, as it’s still performing at a high level.

Regardless, Broadcom is still marching toward that $1 trillion market capitalization figure. From an average of 27 Wall Street analysts, all of them have a buy rating on the stock and predict the stock price will be about $199 one year from now. That’s a 19% rise from today’s price, but that’s not enough to grow the 30% required to achieve a $1 trillion market value.

However, if Broadcom can deliver that level of stock performance, it will likely far outperform the broader market (measured by the S&P 500), which typically grows about 10% annually, making Broadcom an excellent stock pick. If it grows 20% over the next year, it won’t be that far off from the $1 trillion mark and would likely achieve it in 2026 if it can keep up its growth.

With the strong and growing demand for its AI products, Broadcom should see strength for years to come; while I’m not sure if it’s the best AI stock to buy, it’s a strong pick and will likely produce good returns for investors.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet and Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.